A Turbulent Start

2024 so far has been a roller coaster ride for the polymers business from the very beginning of the year. The sudden increase of freight rates in the beginning of the year as the geopolitical event happens in the Red Sea region, raises concerns from shipping companies. Furthermore, Low water in the Panama Canal made some ships take other routes.

Challenges in the First Quarter

Despite many challenges faced, Q1 2024 is going just fine even though expected to be more fluid. The impact of the Red Sea crisis is responsible for this slower market as freight rates rise, forcing many ships to change routes to prevent any unwanted conflict. Tightening supply also plays a major role while the market remains under pressure.

Slow Market in the Second Quarter

Entering Q2, a slow market driven by rising cost prices and supply disruption by key players causes hikes in certain commodity plastic prices, while the market grows slower. The sudden rise of freight rates in Q2, following the crisis in Q1, has worsened the condition, causing deadlocks between producers and users.

Imbalance of Supply and Demand

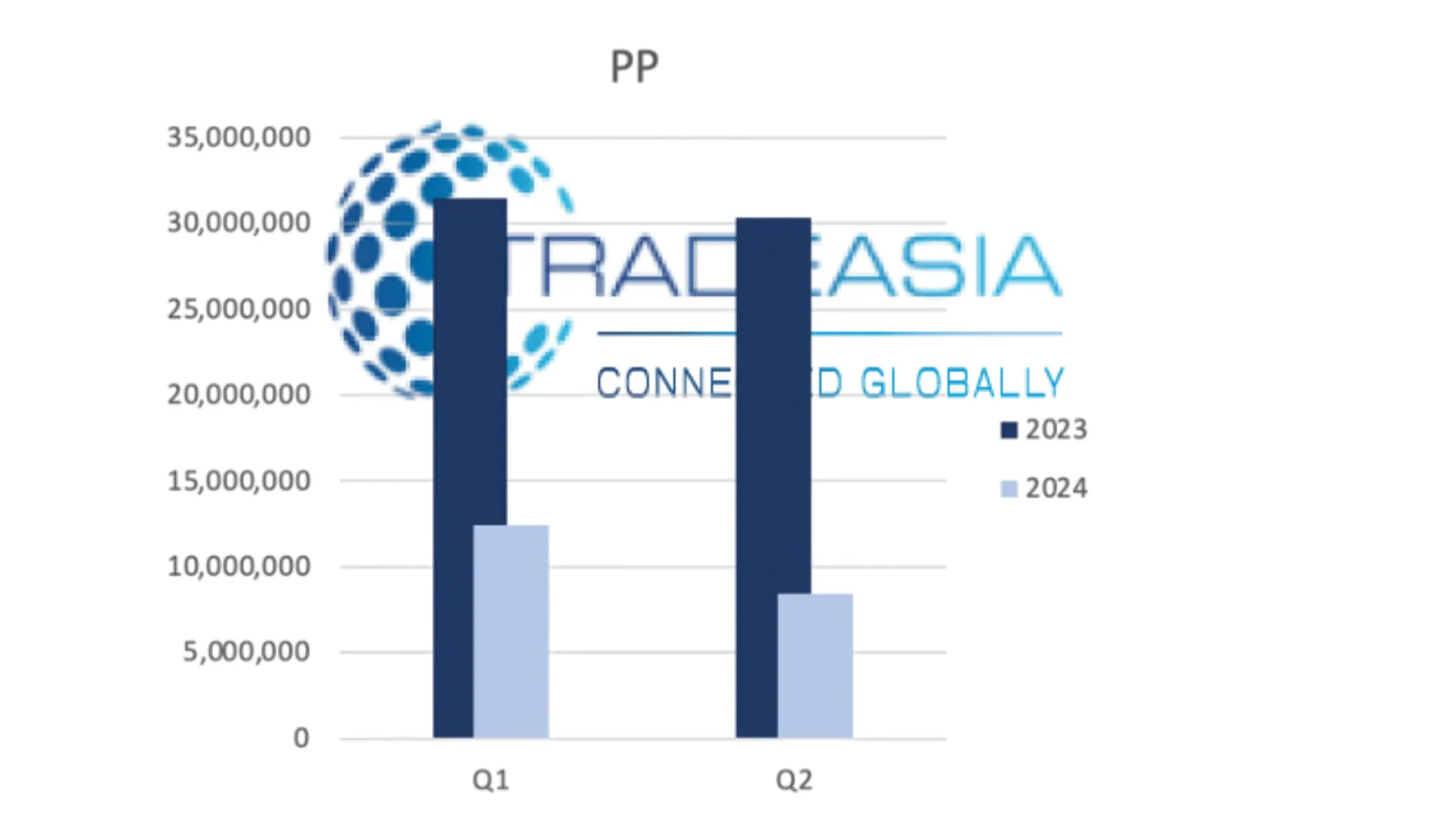

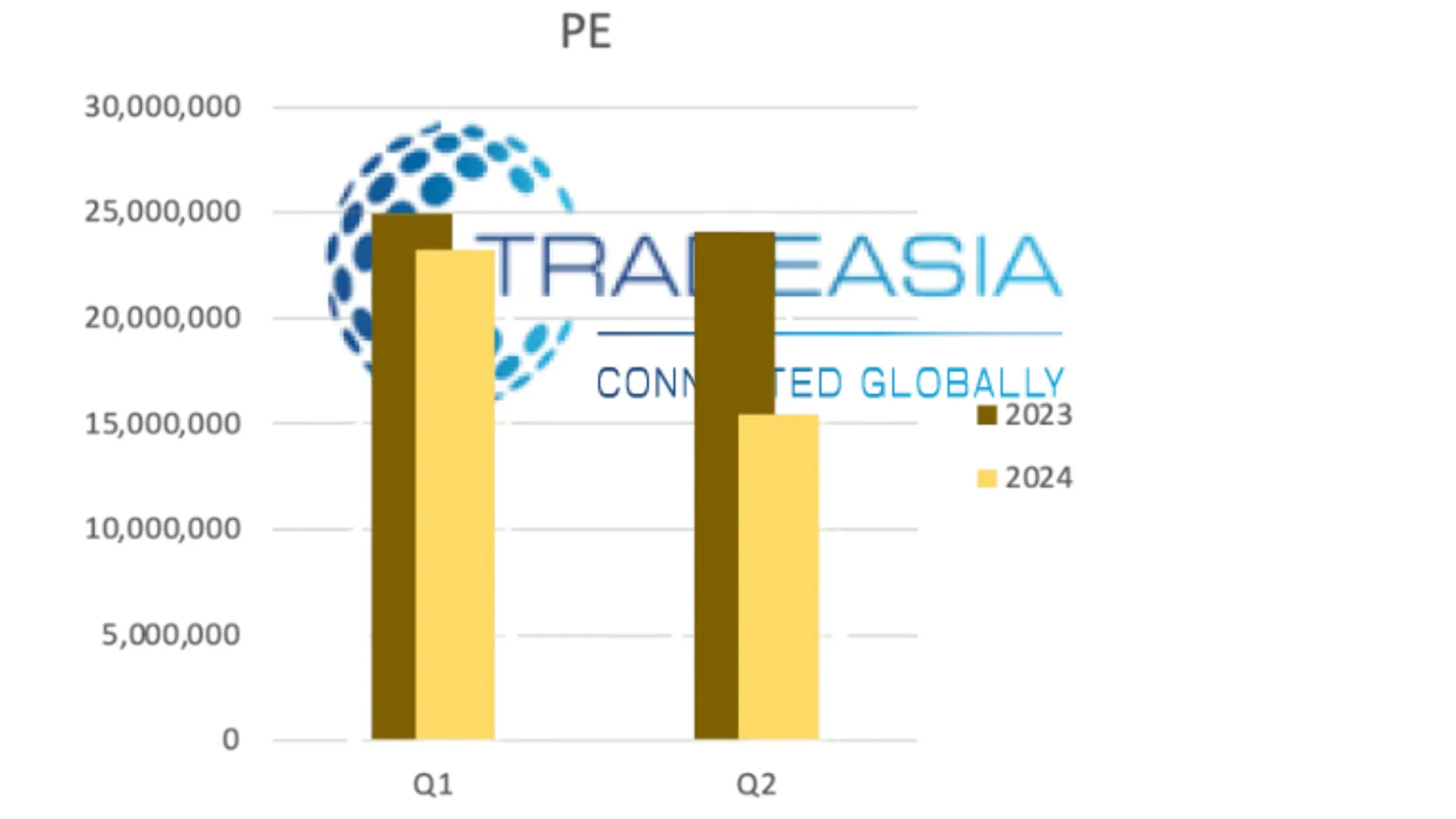

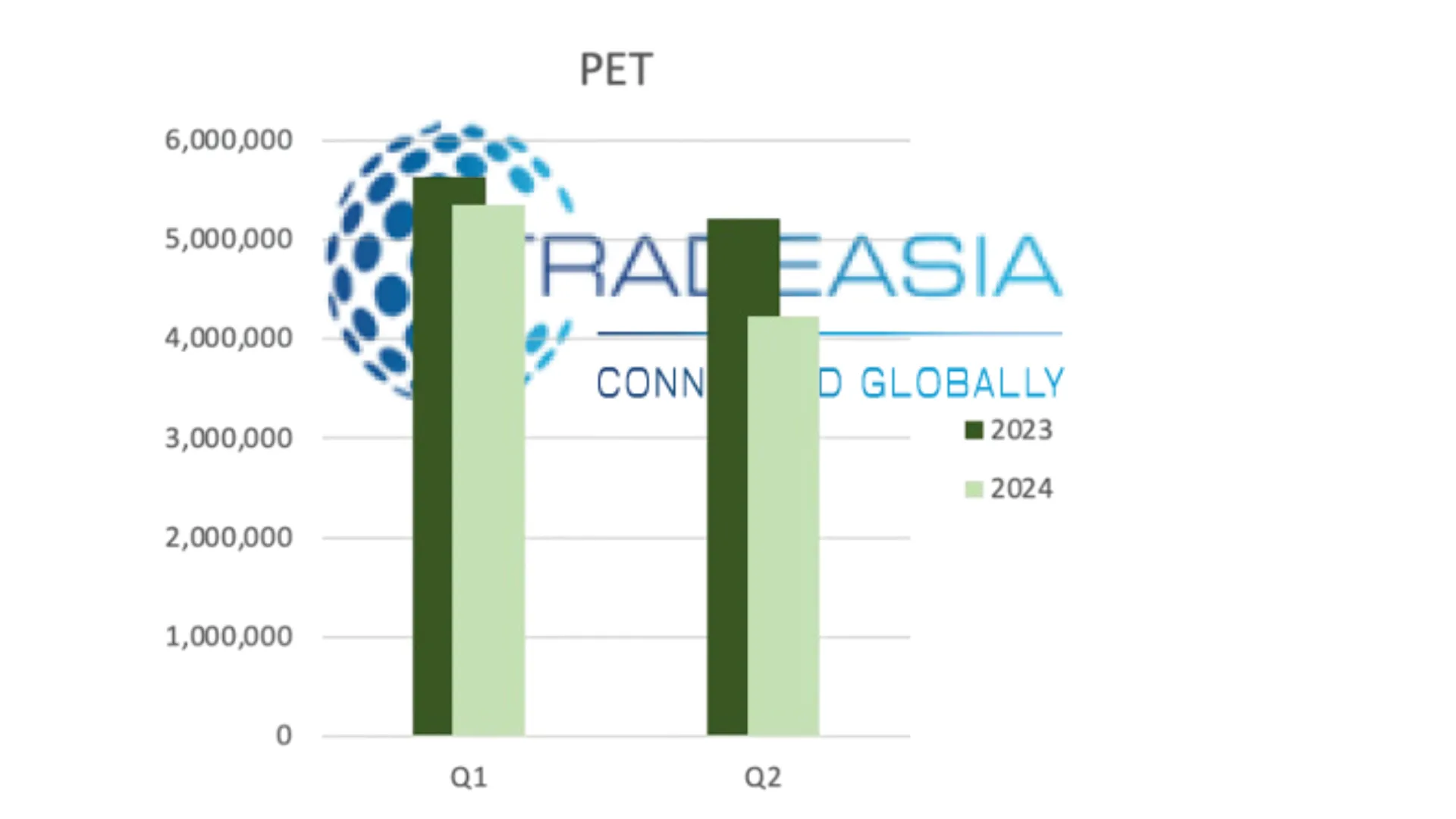

High offers of polyolefins is not followed by the market wills to increase their bids is likely due to sufficient stocks in the market, surging freight rates, and currency level, indicating why the activity in Q1 is better than Q2, despite having similar challenges on the delivery. Our recent study for 4 commodity plastics (PE, PET, PP, and PVC) showed that the first half of 2024 has been very challenging compared to H1 2023.

Significant Quantity Drops

Significant quantity drops shown in the first half of 2024 compared to 2023, particularly in Q2, raising concerns from market participants, when will this condition peak and over. Market players are cautious as supply remains abundant, with domestic and foreign sellers attempting to increase prices despite slow domestic destocking and persistent supply pressure. Though there were reports that several markets have sufficient stocks as mentioned above, the quantity should have decreased since massive buy-outs activity have been seen since Q1 2024, but this also depends on the downstream market activity.

Strategies for the Future

As 2024 has been showing the unpredictable road, we indicate there will be fresh approaches and strategies to overcome these challenges in the future, especially for new comer market participants. We welcome your thoughts and suggestions

Leave a Comment